Uncertainty Disconnects Price And Value

Emotions Vs Uncertainty Vs Reality

When times are tough, as they are now, someone who can articulate and explain the current situation is innately perceived as "smart". Such is the reward for making sense during times of heightened fear and pessimism. Conversely, a person can be outrageously perceived if exercising too much optimism. We ignore salient pessimism when optimism drives profits and detest optimistic opportunity when pessimism fortifies around us.

Optimism and pessimism will ebb and flow because Stocks are affected by so many different things, and the dynamics of investing make it challenging to analyse all the available information, especially if you are a retail/individual investor.

In long-term investing, one must parse between "useful" & "useless "information. Acknowledge the situation without succumbing to negativity and its accompanying emotions that serve no benefit in objective investing.

We are aware of Inflation. It has been a slow grind with everyone watching at the theatre. But how long can one avoid the allure of the market? Especially those enticing bear market rallies. After all, one of those rallies will be the bottom. Eventually, the methodology can succumb to emotion. Human nature is the enemy at the gates of Profit & Loss.

Before we rationalise today's problems, let's explain our behaviours related to investing in the 21st century.

Emotions

I often wonder about technology's effect on financial markets and our interaction. A lot has changed, such as market access, products, information flow, and participation democratisation. However, with more access to information than at any point in human history, we fall prey to many behavioural and innate biases such as Information overload, Expertise bias, or this time is different! These biases often arise from a heuristic interpretation of reality that tends to underserve you as an investor.

But how does this affect our collective awareness as it relates to the information exposed to us, some of which we have no control over as we mindlessly feed our brains?

Being mindful of biases doesn't guarantee negation; identifying them is undoubtedly the correct step.

A haphazard system will leave you devoid of an audit trail and prevent you from analysing the repercussive of your actions. Psychology will help to refine that framework and ask the right questions.

It's best to practise implementing an evolving methodology that structures your actions in the market. It acts as a mitigator against emotion. But, more importantly, it allows your efforts to be auditable and reveals behavioural biases or an innate tilt towards optimism or pessimism.

Implementing an investing framework/methodology is not as complicated as it may seem. It begins with noting every transaction, detailing why you bought or sold, noting any information that helped you formulate that decision, and then questioning through psychology.

Here are some examples:

Expertise bias - Did you give too much weight to an article by a supposed expert, causing you to sell early or miss out on outsized gains? Even worse, you shorted, causing you to lose money.

Action - Scrutinise "expert" information. Try to disprove it. Google the opposite. Most important - Do your due diligence! That way, you learn from your own mistakes and not the mistakes of others. Humility develops investing competence.

Neuroticism - A third of humans possess this personality trait to varying degrees. One pitfall concerning investing is the propensity to overreact to movements in the stock price.

Action - Understand the volatility of your investment—the range of its movement over a year. Think how low or high it could go, then add some more, and if this thought exercise evokes too much emotion, then owning this type of investment might not suit you. Shape your framework to avoid these types of stocks, negating emotional responses.

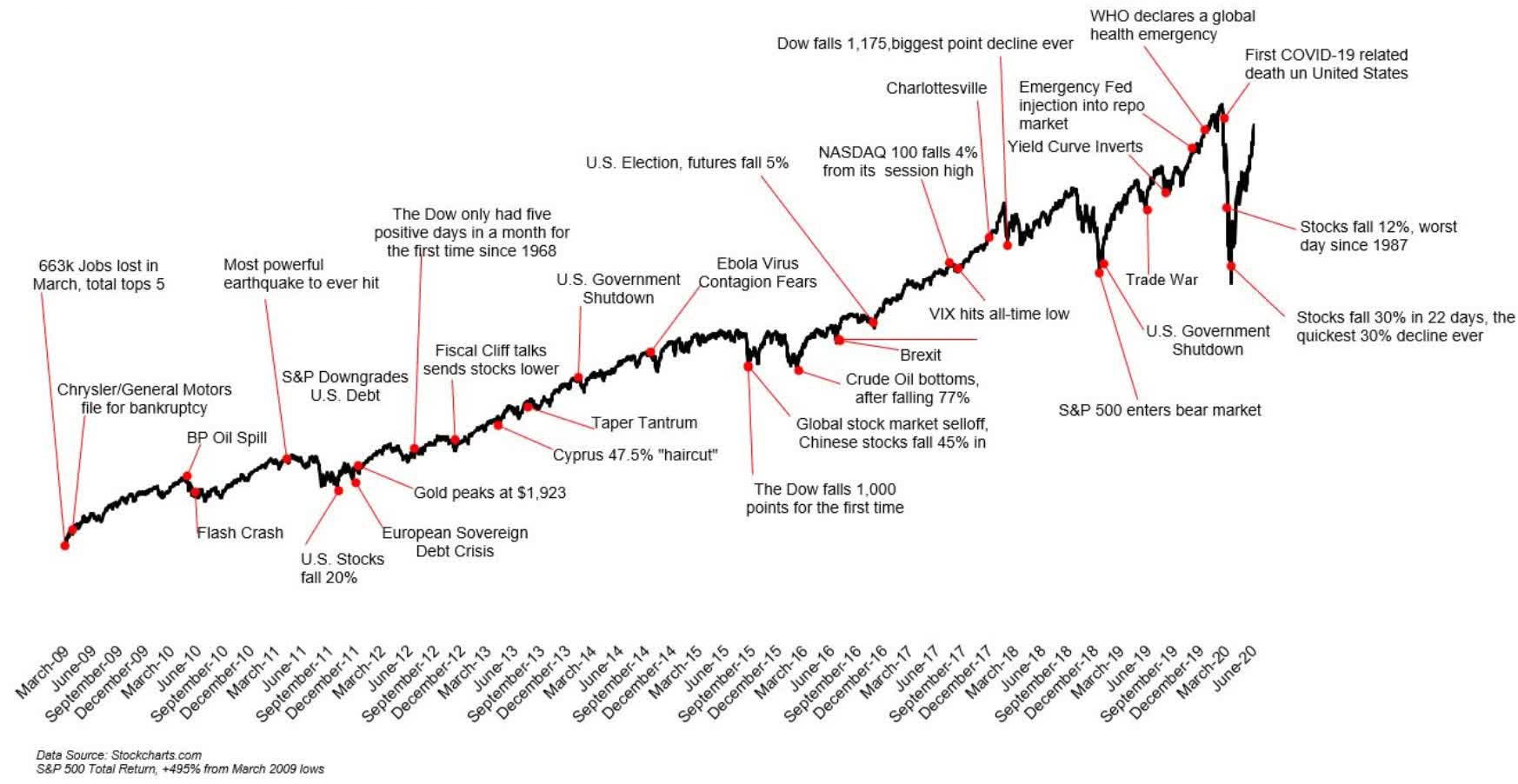

Herding effect - Most prominent in extremes. Everyone sounds "smart" being bearish when all stocks have collapsed; thank you for stating the obvious. Chasing the next "insert current disrupter name" (Tesla, Amazon, Apple, etc.).

Action - Ask yourself; Is 'Herding' making you blind to fundamental value?

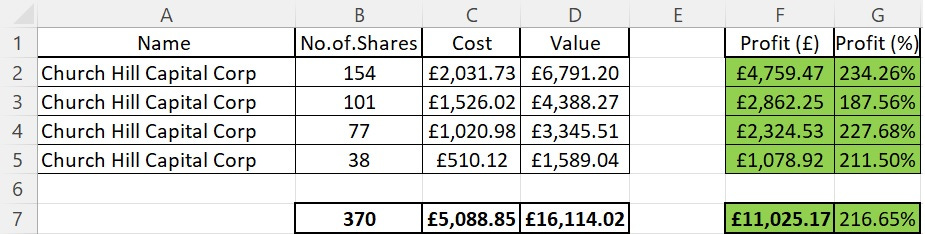

There is no such thing as the "next" Tesla, Amazon, or Apple; however, you can use herding against the crowd. I discovered Churchill Capital, a SPAC, was rumoured to acquire Lucid Motors. It was touted as the next Tesla on Twitter, Reddit, and other forums. I knew herding was intense due to the comparison. Alas, the crowds flocked like sheep. I made a quick trade in about 1-2 weeks.

Keeping records, a journal, diary of your investing and trading is essential. You are not immune to human nature, and great investors are just as susceptible. The difference is they exercise humility and candidly verbalise their pitfalls, allowing them to improve. Interestingly, they kept a record of their actions.

With access to an abundance of information, It's understandable that our innate senses get hijacked, causing us to fall prey to a whole host of biases. Talking about information overload, let's quickly look at where we are now.

Uncertainty

Ultimately, the current situation hinges upon when Inflation will subside. Of course, this will only be evident in hindsight, at which point a new topic will occupy our consciousness. But, anecdotally, when engaging with people in real life or online and curating through the variety of information, I get the inclination that we have some way to go for most people to really "feel" it.

There needs to be more than falling prices alone. The consumer must psychologically feel like they're in a recession to reset expectations. There is conflicting data and mention of the consumer being reasonably healthy despite Inflation running rampant.

The tipping point will be job layoffs, mortgage/loan defaults, house prices falling, and pensions down in value. Pessimism and negativity will eventually impact consumer habits. The consensus of a recession being next year is predictable; I could be wrong. The issue for us investors is that we cannot time bottoms; moreover, markets look forward.

Here is what we do know. First, the FED still has to pivot. A recession still has to be "felt".

If macroeconomists spend their lives trying to guess the mass behaviour of billions and fail for the most part, then I don't have to time the bottom. The road is always unknown, markets look forward, and the unpredictability of life means, for the most part, it can be a futile exercise.

The beauty of the future is the unknown; within that uncertainty, there is hidden alpha to reward those willing to buy and wait. If the value and fundamentals of the company reach your future forecast, then the price will eventually follow.

What information are you focussing on right now? You may be trying to time the bottom and becoming susceptible to 'Regret Aversion', repeating the same mistake repeatedly. Is 'Herding' making you blind to fundamental values?

I am still determining when Inflation will blow over because no one does. However, when times become this uncertain, you can be sure of one thing; Price and value diverge.

Reality

Any market mispricing will take time to be appreciated, and the extra price you must pay is volatility. But, it would be best to remember that staying invested or investing through tough times ensures you catch those rare days when stocks "pop".

Uphold long-term understanding and horizons. Trying to quantify every external factor outside a company's control is futile. Also, we must adapt our thinking and psychology to where we are now.

Previous stock prices, multiples, and their respective moving averages were a product of an environment excess with liquidity and speculation; we cannot expect the same standards to persist. If this is a different environment, then other multiples will apply. Therefore, you must mentally jostle between knowing the environment you currently find yourself in and its accompanying expectations & valuations.

Do you have the mental fortitude to withstand the current price being far from your forecasted future value? Can you stick to a framework that relieves the induction of panic and fear? If not, then you shouldn't be investing. The mechanics of the markets are simple, but predicting them is difficult.

Opportunity

Optimism and disruption are detested in this environment; therein lies opportunity.

The Inflation Reduction Act (IRA) incentivises bringing battery and renewable energy supply chains back to North America. Critical to this is Cathode production—a long and expensive process with a crucial aspect served exclusively by Chinese companies.

There is a North American company that has the potential to disrupt the supply chain and negate the part of the process offloaded to Chinese companies. It has a patent covering its technology. It is speculative but benefits from the IRA. (Expect a write-up soon)

Are there other incentives for other industries? Maybe some companies can provide the picks & Shovels?

Cathie Wood of Ark Invest has stated that the prime time for many innovative technologies was too early in the 2000s. Allow me to adapt this narrative; I agree, but she was slightly off. The time is now.

Inflation forces company's to use innovative and cheaper methods. Companies will employ the person they can pay less but can do the same job as another candidate. So, it's no surprise Companies will deploy software if it does the same job as a whole department. Inflation is most likely discounting, unfairly, some COVID winners.

There will be disruptive stocks with compelling investment stories, but the current hostile environment is miring their potential.

All-in-all, uncertainty breeds irrationality and unpredictability. We are there.

You have to ask yourself three questions:

(1) Does your research reveal the mispricing of individual equities?

(2) Can they survive the current environment?

(3) Are you willing to hold and watch your stocks be negative until an unspecified time allows for margin and multiple expansion?

Case Study

I've owned Nvidia since 2016. My initial purchase has performed well through various situations - Trade war, an Election year, and Pandemics.

In 2018, Nvidia faced bloated sales due to the cryptocurrency miners utilising their graphic processing units; I had to use my framework to understand the potential future impact. For me, I always start with fundamental questions about reality. Will they go bust? How long will sales take to normalise? Will the market punish them in the short term? How long will I watch the stock price go down, and how low?

Quantitively, I always revert to Debt & FCF. It tempers certain negativity biases as it alleviates the concern of bankruptcy.

Being rewarded with outperformance in the stock market requires you to endure the journey. Ensure you have some framework in place, and make sure you are constantly auditing your actions to refine your methodology.

I'm still long NVDA.

Coming next…

Deep dive into qualitative elements that help identify companies that can deliver above-average growth

A qualitative look at Palantir under a series called the ‘Karp Files’

A write-up on a speculative nano-cap company based in North America with patented technology that could disrupt battery manufacturing.