6 Breakdowns in the Disruptive Innovation Process

Understanding Innovative processes

Introduction

Since reading Chris Mayers book 100 baggers, I’ve been inspired to look for factors contributing to innovation and above-average growth.

There will never be a set formula because the world is dynamic; said another way, factors and environments that work in favour of a particular company or disruptor may not apply to another company. That is the crux of investing; Figuring out as much as we can to paint a model of reality that directs our prediction. The future is the judge at the behest of our ignorance.

For this reason, I exercise scepticism when studying white papers, reports, and traditional MBA strategies; having said that, there is always information we can extract and add to our repertoire of knowledge, aiding us in our hunt for above-average compounders.

I came across a white paper breaking down the processes of Disruptive Innovation. As I intimated in my introduction, I don’t heed everything in these types of reports, but they do contain some insight, but you need to extract the information selectively.

I will briefly explain each section, followed by real-life examples and an excerpt from the paper. Let’s look at the six breakdowns.

The six breakdowns

(1) Innovation Zoo: Too many unfocused areas

Essentially, you should be continuously innovating and out-innovating your competitors. The key is figuring out what will work and aligns with the company’s overarching strategy and goals Vs distractions and digressions.

Amazon AMZN 0.00%↑ is a beast when it comes to incepting innovative ideas and making them successful and killing bad ideas likely to flop or that have flopped already.

Do you remember the Amazon fire phone?

What about when they began competing within the in-store payments space against Square SQ 0.00%↑ with a product called ‘Local Register’?

How about when they copied Groupon with Amazon ‘Local’?

Source: Business Insider

Me neither, but I bet you know what AWS is. You most likely have an Alexa at home. And if you’re using Amazon, you're most likely a Prime Customer.

These innovations aligned with the company’s core values and strategy. Amazon quickly understands what projects it should continue to push and invest in and what ones to cut off completely.

Source: Think Monster

Here’s an excerpt from the White Paper;

“If you are investing a little bit in everything, you likely are not investing enough in anything, forfeiting the opportunity to support your best bets. Ideas may demonstrate promise, without the executive sponsorship needed to incubate and scale….The fix is simple: put boundaries around employee ideation so that it is more tightly aligned with the firm’s strategic intent, resources, and core competencies.”

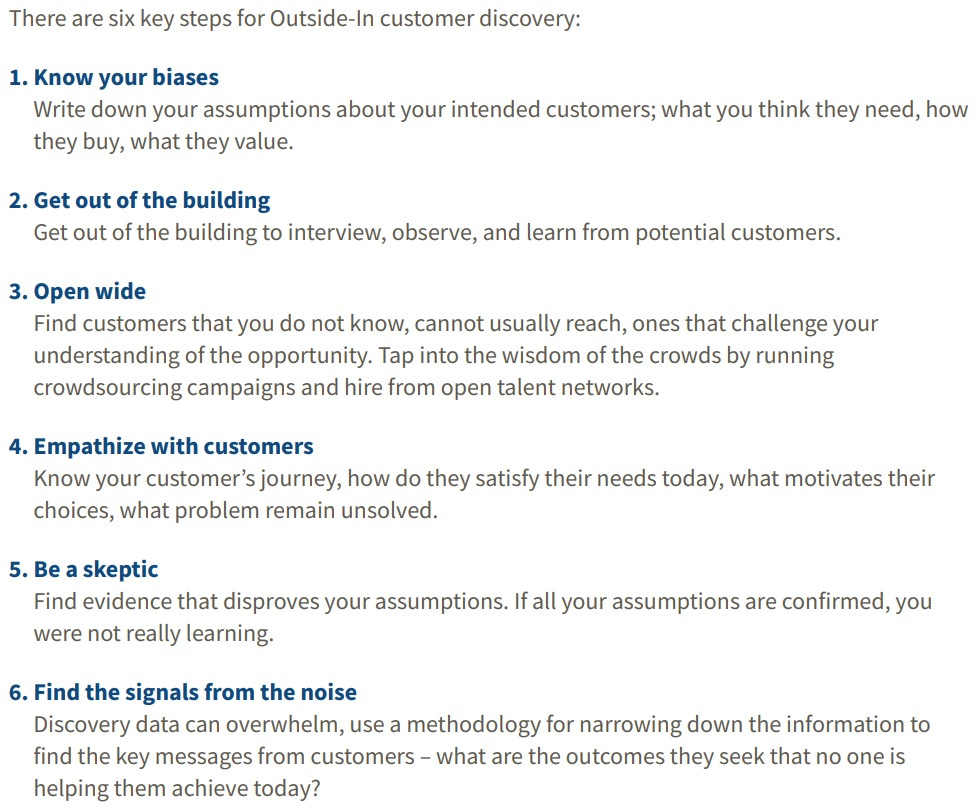

(2) Inside-Out: Failing to test your ideas with customers

It’s about taking ideas and validating them with customers before doubling down and going full steam ahead. Failing to validate an idea could waste resources and time, but at worst, it could end your business.

Unilever UL 0.00%↑ owns one of the most successful beauty brands - Dove. In 2017, they released packaging for their shampoo in various shapes and sizes meant to represent the different bodies of women. They didn't validate the idea and were publicly lambasted. Dove is still around today, and its credibility has been restored; however, if they were a young standalone company, this could have been its detrimental end.

There is one caveat - Customers and consumers don’t always know what they want. This was best exemplified by Apple AAPL 0.00%↑ under the reigns of Steve Jobs.

Before the iPhone launch, many surveys and consumer feedback indicated a low appetite for this type of smartphone. I need not tell you what happened because you’re most likely reading this from an Apple Smartphone.

This may astound some people because we are used to the multi-capable phones of today, but do not underestimate the incredulity of human behaviour. The term Luddites didn’t arise from fiction.

I digress, and I cannot find the original survey, but here is a link to a publication that captures the general incredulity at the time - Article.

We could lazily attribute this to luck if it weren't for Apple AAPL 0.00%↑ pulling this off again, this time with Tim Cook at the helm. The Apple Watch was not received well, with over 80% of people stating they would be ‘Not so likely’ and “Not at all likely to purchase the product, according to one survey.

The business lesson here is always to test and validate new ideas with your core customers unless you are Apple. Focus on what excites customers and connect with them emotionally unless the company creates a product that consumers do not know they need yet.

Guessing what the consumer wants before they know is one side of the game; you then have some companies that guess what businesses need before they know themselves.

Palantir PLTR 0.00%↑ had developed software they often tout as being developed for tomorrow, made before organizations realize they require it. When the pandemic came around, they deployed their software in the UK & USA in record time and rolled out one of the quickest and most efficient PPE & vaccination programs.

Here’s an excerpt from the White Paper;

“Engaging customers directly helps you learn which of your assumptions are true and which are self-serving. Innovators that know what delights customers are better placed to create an emotional connection that excites end-users and generates competitive advantage.”

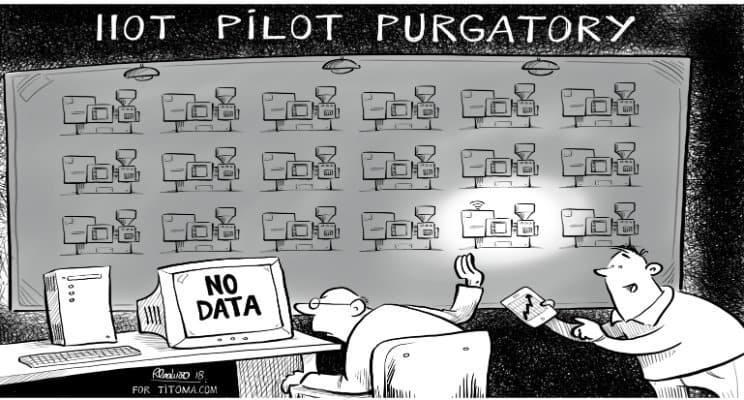

(3) Pilot Purgatory: Outside-in customer discovery

This one sounds like a combination of the movies Top Gun’ and ‘The Purge’. I can assure you no pilots were killed in the summation of this business concept.

In all seriousness, this is when a business comes up with a new way to enhance its value proposition or improve the business, but the idea never makes it out of ‘pilot’ mode.

It tends to occur when businesses are doing well, and management uses excess resources and cash towards proof-of-concept ideas or technology proof points. I’ve always opined that it’s a way for CEOs and management to impress shareholders and investors by exploring and experimenting with the current ‘hot’ technology and masquerading as being innovative when in reality, there is no real intention to see the idea of deployment or no defined route as to how it will deliver ROI; Vanity over reality.

The reasons for failure can include the following:

The internal ecosystem doesn’t support it

Unable to contain approval from external vendors

Company policy roadblocks the idea.

Do you remember the hype of AI (Artificial Intelligence) and ML (Machine Learning)? How many pilot programs were implemented? How many programs contributed to financial metrics?

How about IoT? Many companies trialled sensors and other IoT devices, but only a few see it to full deployment.

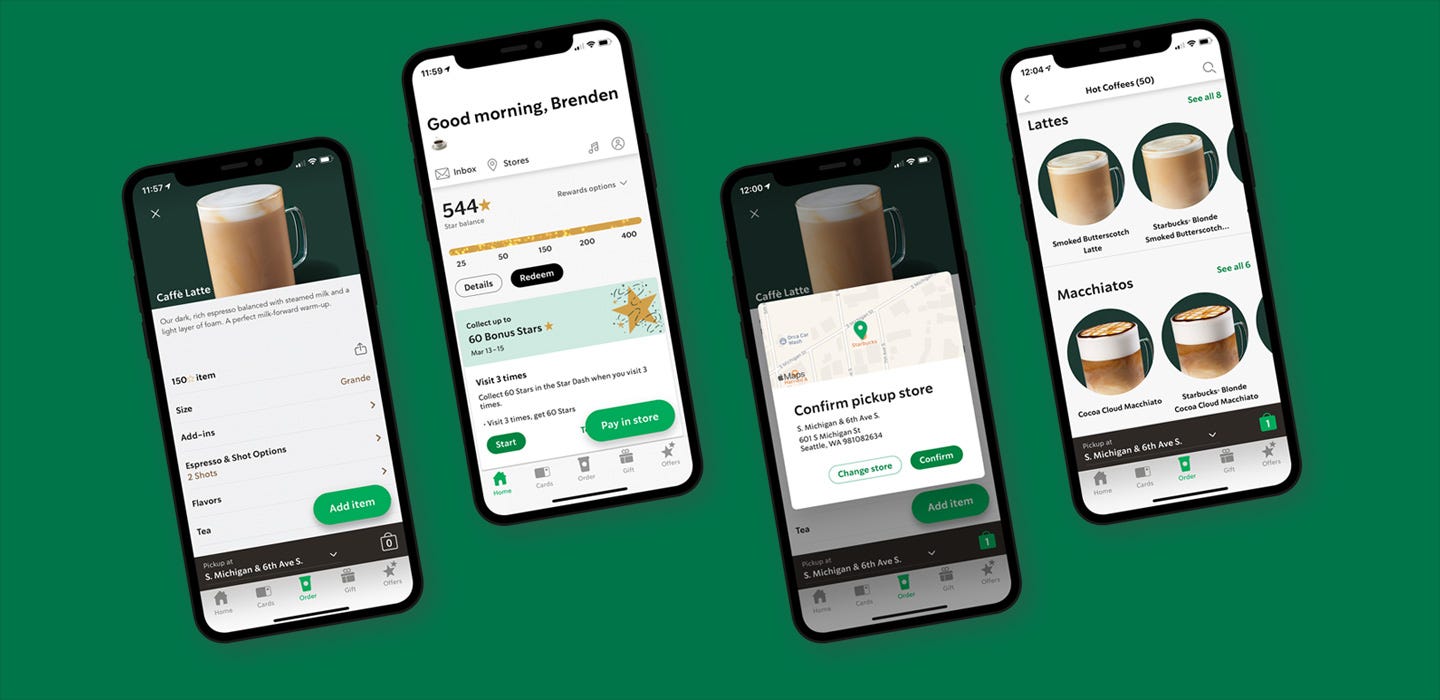

But not all companies and organizations suffer from the purge. Some are master deployers of pilot programs. Here’s an excerpt from this source regarding Starbucks’ S 0.00%↑ and its “In-App Order-Ahead” program.

“The firm was also a mobile order-ahead pioneer. The chain began pilot testing pre-ordering back in 2014, when the concept still required explanation, and when the feature’s very existence made headlines industry-wide. Now, the ordering method is a staple for most major QSR chains. In addition to minimizing time spent in store during the pandemic, the feature also meets consumers’ expectations for convenience and immediacy. Even then, the feature was in high demand, evidenced by its move from pilot test to nationwide rollout in record time.”

As you read the source, you will discover more programs rolled out successfully, but the most impressive thing is the adoption of new technology. They don’t use buzzwords; they implement them.

Here’s an excerpt from the White Paper;

“Projects that start with the problem statement of how we can apply this technology, are doomed to Pilot Purgatory. Start instead by defining a measurable opportunity gap. Unless you have a sense of the magnitude of the problem you are solving and the breadth of the opportunity, there is no motivation for continuing, even after a successful pilot.”

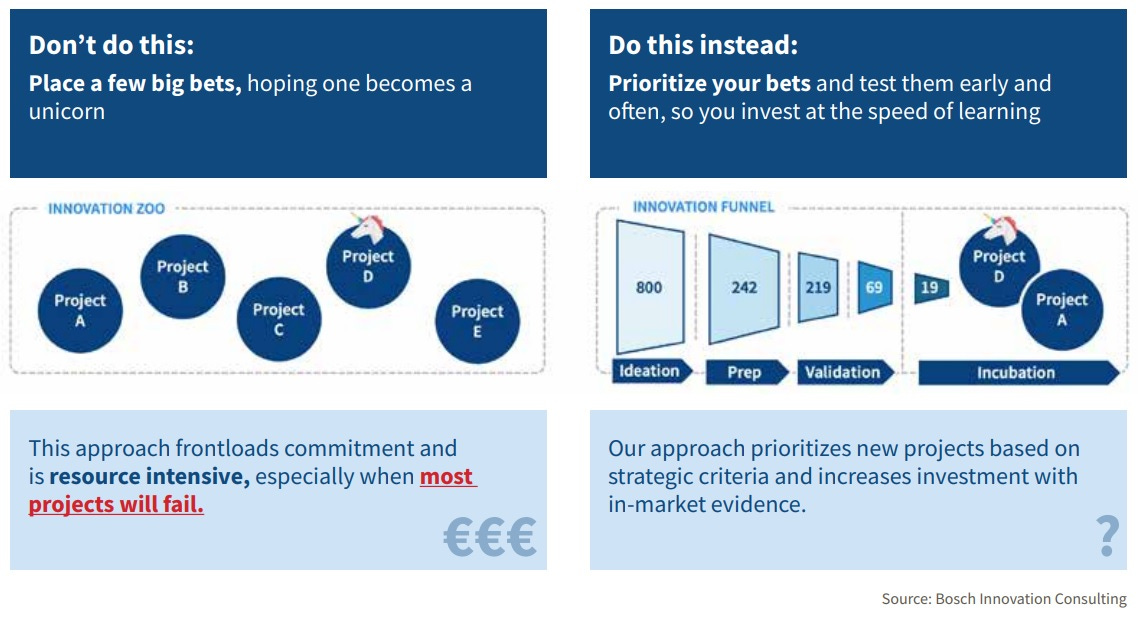

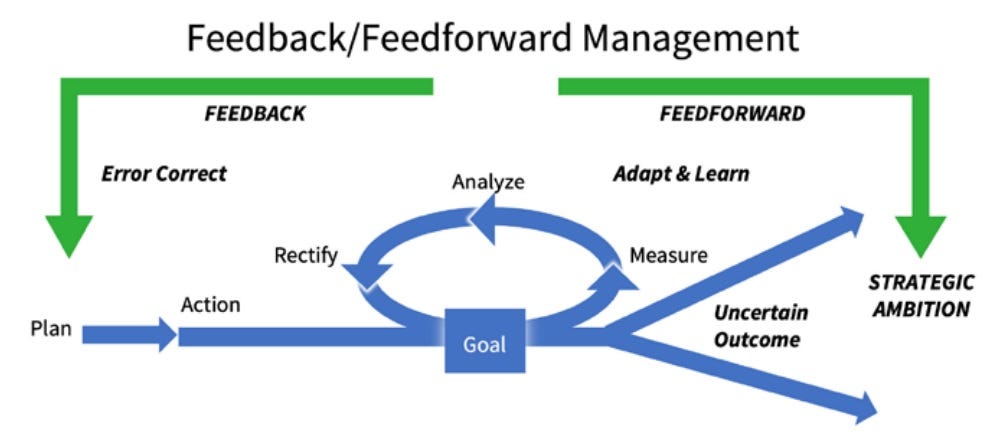

(4) Investing ahead of learning: Graduating a new venture too soon

This is the classic innovator’s dilemma. It’s about exploring and substantiating innovation and ensuring it’s informed rather than implementing a new product or setting up manufacturing without knowing if it will work, who the end customers are going to be, or if it’s a good idea.

Executives and managers succumb to operational performance where they are expected to know what the solutions are, but if you act and think like a start-up, then you need to be driven by agility, not speed.

There is a perfect example of this in the report regarding General Electric $GE and its plan of becoming a ‘Top Ten’ software company that ended in epic failure.

“In 2014, GE’s digital transformation vision was bold. It saw the possibility for the ‘Industrial Internet of Things’ and set itself the goal of being a ‘top ten’ software company. They anticipated sensors gathering data about every aspect of a manufacturing plant’s operation being fed back and analyzed in the Cloud in real-time. These ‘smart machines’ would radically improve effectiveness and efficiency for thousands of companies world-wide. They forecast a market worth $500 billion by 2020 and committed to create a first-mover advantage. GE tripled its R&D budget, built a 1,000-person software division, and launched its own big data platform--Predix. Five years later it had failed. They built a universal big data platform, when the market wanted a way to process existing data for specific applications. They invested without confirming the customer problem and the customer’s willingness to pay for it. A new CEO closed down the strategy, the legacy business reasserted control, and GE’s ambition to be a software firm folded.”

If a company is setting out to invest in a new area of growth far removed from its original offering or deviating from a tried-and-tested method of selling to its core audience, then question how much learning they have done and its ability to be agile over being able to deliver at breakneck speed.

If they have done their homework and have iterated according to what they have learned, then, by all means, they can push forward with all their resources. A failure to learn and be agile is a sure path toward failure.

Here’s an excerpt from the White Paper;

“We talk a lot of talk about creating ‘fail fast culture. However, the goal is not failure, it is rapid learning. When you learn, you can make faster, more informed decisions… It is not speed, it is agility... Impatience drives decisions that are not based on evidence, leaving the company vulnerable to committing to a business model that may not work. ”

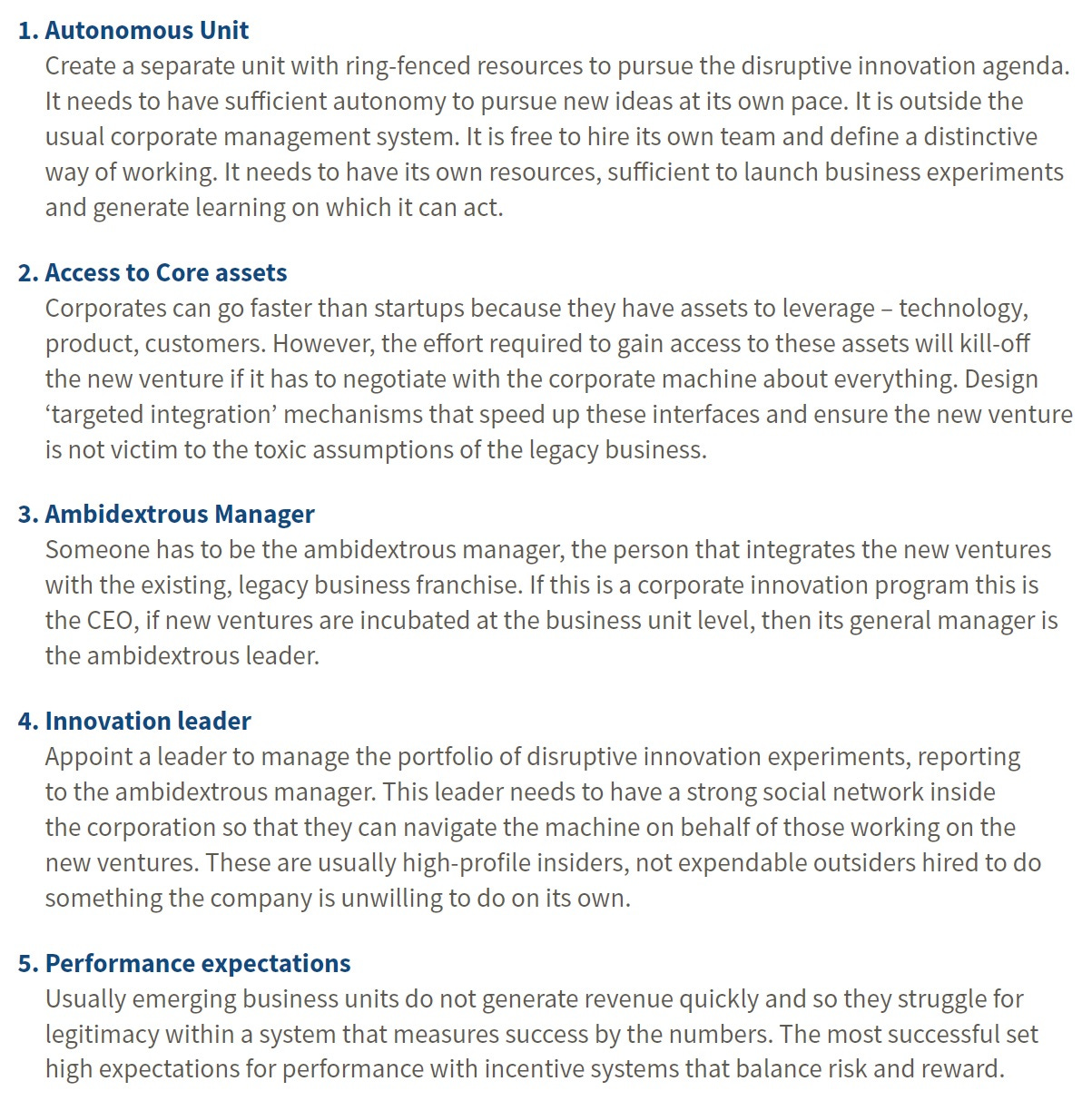

(5) Crossing Wires: Failing to separate explore from core business

In short, if you have a highly successful core business but want to explore a new business avenue, it is best practice to separate the two.

The reason for exploration could be many such as:

The threat of being disrupted

A risky but obtainable new business avenue

To mitigate the contagion effects of failure from exploring new business opportunities.

Satisfy shareholders and investors.

An excellent example of this is Volva, and it’s subsidiary Polestar. Whilst not organically incepted from within the organization, management’s decision to operate it separately, affording it autonomy and an exploratory business model whilst still giving it access to Volvo’s core assets, is a master class in how to separate from the core business and make it successful successfully.

Of course, Electric Vehicles are nascent, and anything can happen, but so far, Polestar is shining fairly bright.

Polestar was founded in 1996 and originally incepted to help manufacture a race car that would boost the Volvo team’s chances of winning the Swedish Touring Car Championship (STCC). They were originally known as ‘Flash Engineering’.

After finding success in racing, other innovations and vehicles were developed, helping Volvo continue its success in the automotive industry. Notable models include the S40, S60, C30 and V60, some of which are still being produced and upgraded.

In 2017, Polestar’s goal and purpose changed to being an electric performance car brand.

They are now public under the ticker PSNY 0.00%↑ and delivered $1.34 Billion of revenue in 2021. Volvo owns 49.5% of the company.

If you want to explore a new business avenue that is materially different from the core business, then it may be easier and less of a distraction to completely separate so it can enjoy all the advantages of being a start-up not encumbered by the old business whilst still having access to resources and assets giving it the best chance to survive and thrive.

Here’s an excerpt from the White Paper;

“An Explore business unit has a different rhythm. It lives with high uncertainty… Core businesses drive to short-term results so that they can meet performance expectations… The solution is an ambidextrous organization that separates Explore business out from the Core… Explore needs autonomy to operate…”

(6) Capacity to act: Not committing resources to a new venture.

This aspect is far too similar to number (3) Pilot Purgatory and (5) Crossing Wires with highlights of (1) Innovation Zoo.

The fundamental lesson here is aimed at management and executives wrestling with a new idea that may cannibalise the current business.

Coming soon…

A qualitative look at Palantir under a series called the ‘Karp Files’

A write-up on a speculative nano-cap company based in North America with patented technology that could disrupt battery manufacturing.